According to a report by Grand View Research, the global industrial hemp market size was estimated at $6.45 billion in 2024 and is expected to grow at a CAGR of 17.5% to reach nearly $17 billion in 2030. In 2024, the hemp fabric (textile) segment remained the leading application area, capturing around 24% of the market, fueled by increasing adoption in sustainable fashion and eco-friendly apparel production. This was followed by other major segments including food and beverages, construction materials (such as hempcrete), and cosmetics and personal care products.

In addition to its industrial uses (such as fiber and grain), hemp can also be used to derive CBD. Cannabidiol (CBD) is one of the numerous compounds found in the cannabis plant. CBD oil can be obtained from two different species of cannabinoids: marijuana and hemp. Hemp-based CBD oil products have a lower delta-9 tetrahydrocannabinol (THC) concentration, while marijuana-derived CBD oil products have a relatively high concentration of THC.

Therefore, it is more likely that a prescription from a doctor will be necessary to acquire marijuana-based CBD products rather than hemp-based CBD oils, making hemp-derived CBD products much more accessible to consumers which in turn contributes to greater demand for them. This is particularly visible in the share that hemp-derived CBD products occupy in the U.S. CBD market – the largest CBD market in the world currently.

The global CBD market size was valued at approximately $9.8 billion in 2024 and is expected to grow at a CAGR of 15.2% from 2025 to 2030, reaching an estimated $23-25 billion by 2030. In 2024, hemp-derived CBD dominated the CBD market, accounting for around 57.2% of total CBD sales. According to updated estimates (based on Grand View Research and other industry sources), the global hemp-derived CBD market reached $5.6 billion in 2024, up from $4.3 billion in 2023 and $2.7 billion in 2022. B2B segment accounts for the largest revenue share. Hemp-derived CBD is legal in at least 57 countries with varying regulations.

These days, at least 70 countries cultivate hemp for commercial or research purposes. In 2024, hemp acreage in North America and the European Union countries totaled around 82,000 acres and 88,000 acres respectively, while China – the world’s largest hemp fiber and seed producer – planted around 95,000 acres of hemp which brought the global acreage to over 270,000 acres.

Australia, New Zealand, Germany, the Netherlands, Paraguay, Uruguay, Chile and South Africa are also among countries with active industrial hemp markets. Regulatory developments in Latin America and Africa are expected to open new opportunities for hemp-based CBD exports while Japan and South Korea represent emerging markets in this industry.

The THC limits set for industrial hemp differ between countries. The most commonly found limit is that there must be no more than 0.3% THC in industrial hemp – this is adopted by Canada, USA, most countries in Europe, Chile, China, Lesotho, Morocco, Rwanda, Uganda and several others. However, some countries choose a lower limit of 0.2% such as the United Kingdom. On the other hand, several countries have adopted higher limits. For instance, in Australia, New Zealand, Costa Rica, the Czech Republic, Ecuador, Malawi, Mexico, Switzerland, Uruguay and Zimbabwe, the THC limit is 1%. In South Africa, the THC limit is even higher at 2%. Meanwhile, South Korea and Japan have very strict regulations which state that hemp must have 0% THC with only trace amounts allowed.

Hemp-derived CBD is legal in at least 57 countries with varying regulations. In some countries like Sweden and Latvia hemp-derived CBD cannot have any THC. In USA, regulations on hemp-derived CBD differ depending on the state. In Canada, hemp-derived CBD can be sold only by cannabis retailers and cannabis regulations govern hemp-derived CBD. In New Zealand and Australia, hemp-derived CBD medicines require a prescription with the exception of low-dose CBD medicines which have been reclassified since October 2023 as pharmacist-only medicines.

US & Canada

North America is the largest regional market for CBD with an estimated value of $7.9 billion in 2024, driven by the U.S. – the largest single CBD market in the world the growth of which is fueled by widespread legalization at the state level, a robust wellness industry and strong consumer demand for hemp-derived products. The region is also responsible for around 30% of global hemp cultivation.

Canada on its own accounts for around 13% of global hemp cultivation. Since hemp cultivation was legalized in Canada, production has been variable year to year but generally increasing – which some attribute to increased import demand in the United States. For instance, in 2022, over 90% of exports of hemp from Canada were made to the United States.

The Canadian Cannabis Act cleared the way for whole hemp plant utilization. Though industrial hemp licensees may not extract CBD themselves, they can sell hemp leaves, flowers and branches to a holder of a cannabis processing or research license who can then extract CBD from them. According to the most recent data from Statistics Canada, the seeded area of hemp was about 62,000 acres in 2021, 76,900 in 2022 and 55,400 acres in 2023.

In 2024, 36,572 acres of industrial hemp were planted, with about 14,000 acres seeded in the Manitoba province.

It is estimated that sales of hemp in Canada were around $525 million in 2022. Market estimates for the value of hemp-derived CBD in Canada are limited, but researcher Jan Slaski of InnoTech Alberta has predicted that the overall Canadian hemp industry could be worth $1 billion a year.

In December 2018, the Farm Bill was signed into law to make hemp legal for the first time in the United States since the 1930s. The bill removed hemp from the Controlled Substances Act. The passage of the Farm Bill had a dramatic effect on the area intended for hemp cultivation in the U.S. – in 2018, it reached 78,176 acres, tripling from the 25,713 acres in 2017. In 2019, the number of acres licensed for hemp cultivation skyrocketed to 500,000, though only 230,000 acres were actually planted and yields totaled 115,000 acres. However, due to oversupply in the market, in recent years the number of licensed hemp acres fell to only 45,000 in 2023, with more than 27,680 acres planted and 21,079 harvested (up 15.5% from 2022), according to the National Hemp Report 2024. Latest USDA data reveals that there were 5,532 active licenses and 45,294 acres planted in 2024 – up by 63.6% from the previous year. The acres of hemp harvested also increased considerably by 55.1% to 32,694 acres. Hemp floral varieties accounted for about 36% of total harvested acreage, fiber for 58%, grain for 15% and seed for 7%.

The value of hemp production in the open reached its peak of nearly $1.2 billion in 2019. After a consistent negative trend in the following years, falling to $212 million in 2022, in 2023 the value of hemp production in the open rose by 21.7% to $258 million and then further by 61.6% to $417 million in 2024 – showing the industry’s recovery. These figures are taken from National Hemp Reports which, when estimating the value of hemp production, take into account sales of raw hemp material only and not finished hemp products. Total hemp-derived products are projected to reach $5 billion by 2028.

After the adoption of the 2018 Farm Bill, CBD producers have had a much greater incentive to use hemp as their main source for CBD. Though hemp-derived CBD sales did decline in 2021 and 2022, they began to rise again in 2023, reaching nearly $1.7 billion in 2024 and are projected to hit close to $2 billion in 2025.

Grand View Research projects that total sales of hemp-derived CBD consumer products in the U.S. will grow at a CAGR of 13.8% while hemp-derived CBD is expected to grow at a CAGR of over 15% post pandemic owing to increasing demand from the pharmaceutical sector and rising awareness among consumers regarding health.

More recently, in 2025, the federal hemp regulations were changed by a spending bill which was approved by President Trump on November 12, 2025. The spending bill includes language that limits total THC (including THCA) in hemp products to 0.3% and bans synthetic/non-natural cannabinoids, effective from November 12, 2026. This closes what is described by some as the “intoxicating hemp loophole” that has allowed high-THC flower and hemp products with chemically altered or synthesized in lab compounds derived from hemp biomass to enter the market.

On December 18, 2025, President Trump signed an executive order, directing to redefine hemp-derived CBD products to allow full-spectrum CBD and to establish a new regulatory framework – potentially revising the spending bill’s rules before they even take effect. The executive order also calls for the development of research methods and models to evaluate the medical risks and benefits of CBD, reflecting growing acceptance of CBD in therapeutic contexts and signaling progress towards clearer, science-based regulations.

Europe

In recent years the area dedicated to hemp cultivation has increased significantly in the EU from 20,540 hectares in 2015 to 25,000 hectares in 2023 and 2024. In the same period, the production of hemp increased by 84% from 97,130 tonnes to 179,020 tonnes. France is the largest producer, accounting for more than 60% of EU production, followed by Germany (20%) and The Netherlands (6%).

Europe is expected to be the region with the fastest growth in its CBD industry over the next 5 years. European consumers are becoming increasingly aware of the health benefits that CBD offers and this has contributed to CBD’s rising popularity. However, the CBD market still faces difficulties in the region such as the classification of food products containing CBD (including hemp-derived CBD) as “novel foods” which prohibits the placement of CBD food products on the market before receiving an authorization from the European Commission. The novel food classification applies to CBD products in the UK as well and UK’s Food Service Agency (FSA) is responsible for issuing novel food authorizations. However, in 2022, the European Food Safety Authority put the CBD food product authorization process on hold due to data gaps and uncertainties relating to CBD intake. The process is still on hold to date.

UK has been slightly more progressive with the use of CBD in food products. Some CBD food products have already received positive safety assessments and have moved on to the risk management stage after which the FSA will make recommendations to Ministers across Great Britain on authorizing these products. According to a statement from the FSA, it plans to make first recommendations to Ministers in Spring/Summer 2025.

The value of all hemp-based product markets combined (CBD, hemp bioplastics, insulation, hemp concrete and other) in Europe was estimated at €1.62 billion in 2020, and is expected to reach €6.3 and €8.8 billion in 2025 and 2030 respectively. The total EU CBD market was estimated at €347.7 million in 2023 and is projected to grow at a compound annual growth rate of 25.8% to reach €1.7 billion by 2030. The two biggest markets for CBD are Germany (€76 million) and the UK (€72 million).

Alternatively, if the European CBD market grows at a faster pace, it could reach €2.6 billion by 2026 with around 50 million users, as highlighted in a report by the Prohibition Partners.

In September 2025, the European Parliament’s Committee on Agriculture and Rural Development voted to adopt an amendment which includes hemp flowers as a licit agricultural product in the EU, moving towards whole hemp plant utilization. However, these new rules still have to be confirmed by the Council and the Commission.

Oceania

The industrial hemp market in Oceania is evolving into a high-growth industrial sector in the region, driven by progressive regulatory reforms and rising demand for sustainable construction solutions and nutrition. The industrial hemp market in the region is projected to reach US$115 million by 2030.

After peaking at 4,132 hectares in 2019, Australia’s planted hemp area declined steadily, falling to 1,493 hectares by 2023 – less than half the area in 2019. This trend reversed sharply in 2024, with plantings rebounding to 3,266 hectares. This resurgence was driven by fibre-focused cultivation which nearly doubled in planted area from 2023 to 2024, and the tripling of hectares dedicated to growing for grain. New South Wales accounts for more than half of Australia’s total hemp plantings.

According to data from the Food and Agriculture Organization of the United Nations, it is estimated that 3,600 tons of hempseed and 12,600 tons of true hemp were produced in Australia in 2023. Australia’s hemp fibre industry is valued at AU$5.4 million while the hemp grain industry is estimated to be worth AU$5 million. Separately, the Australia Industrial Hemp Alliance estimates that the Australian hemp food market has a retail value of $15 million.

A major catalyst for the hemp industry came in April 2017, when the Australia New Zealand Food Standards Code was amended to permit the sale of food products derived from hemp seed that do not contain cannabinoids apart from trace levels. One consumer survey by the University of Adelaide found that 26% of respondents have already tried purchasing hemp food or beverage products and with further consumer education, this proportion could increase as 46% among non-buyers cited unfamiliarity with hemp as the primary barrier.

Initially, an industrial hemp license was required to cultivate, harvest and/or process industrial hemp in New Zealand but on December 11, 2025, a reform of the country’s industrial hemp regulations was announced – eliminating the license requirement and lifting the THC limit from 0.35% to 1%, among other changes.

It is estimated that the New Zealand hemp industry is worth $10 million (as of 2025) and could grow to $30 million by 2030.

The New Zealand Hemp Industries Association however, has stated that the removal of regulatory barriers for industrial hemp in New Zealand can result in total earnings for New Zealand of NZD$2 billion by 2030; this consists of NZD$183 million in seed products, NZD$317 million in fiber products and NZD$1.5 billion in hemp nutraceuticals containing cannabinoids. In addition, 20,000 new jobs would be created in the country.

The construction sector represents one of the largest potential markets for industrial hemp in New Zealand. According to a report from Venture Taranaki, based on the value of the new houses consented in New Zealand in the year ending February 2022, if hemp materials obtain a market share of 0.1%-0.5% in the building materials sector, this could add $19 – $95 million in revenue to New Zealand’s hemp industry.

Vanuatu and Fiji have also legalized industrial hemp. Vanuatu is in the process of developing amendments to its hemp and cannabis law which aim to bring greater regulatory clarity and encourage banks to work with licensed hemp and cannabis businesses, facilitating investment into the two industries.

Latin America and the Caribbean

Since 2013, several Latin American countries have legalized the production of industrial hemp, including Argentina, Colombia, Costa Rica, Paraguay, Ecuador and Uruguay.

The size of industrial hemp area in Latin America and the Caribbean is estimated at approximately 10,000 hectares in 2023 and is projected to reach 50,000 hectares by 2030. In the second edition of the Latin America and Caribbean Cannabis Report – produced by London-based advisory group Prohibition Partners – the cannabinoid-based products market in the region is projected to reach over $500 million in the coming years with over 50% of CBD products sales.

Paraguay started growing hemp in 2019 and is the largest producer and exporter of hemp in Latin America. It is estimated that approximately 2,500 hectares of hemp were cultivated in Paraguay in 2022 by around 350-400 farmers. The hemp produced was used mostly for food and flower, and some for fiber.

Another major producer in the region is Ecuador which reported in 2025 that 2,377 hectares were registered for hemp cultivation in the country.

Currently, hemp/CBD products are commercialized in Brazil, Mexico, Bahamas, Bermuda, Antigua and Barbuda, Aruba, Trinidad and Tobago, Colombia, Ecuador, Costa Rico, Peru, Paraguay, Chile, Uruguay, Argentina.

Africa

Currently, 11 countries are reported to allow the growing of industrial hemp in Africa, including Botswana, the Kingdom of eSwatini, Ghana, Lesotho, Malawi, Morocco, Rwanda, South Africa, Uganda, Zambia and Zimbabwe. Most of these countries have set the THC limit for hemp at 0.3%, the same as in the United States and Europe, but Malawi and Zimbabwe set the limit between marijuana and hemp at 1.0%.

South Africa made a major step towards boosting its hemp industry when in December 2025, the Department of Agriculture announced the commencement of the new Plant Improvement Act which raises the THC limit in hemp’s leaves and flowering heads to 2% bringing the law into better alignment with the country’s agronomic environment. As of September 2024, South Africa has issued over 1,000 permits for hemp cultivation since hemp was declared an agricultural crop in the country.

The Hemp Business Journal estimates hemp retail sales in African markets at $133 million in 2022.

A report from Africa Hemp Fund projects that in the future the African industrial hemp market (excluding CBD) could be worth US$2.4 billion annually and create 180,000 job opportunities on the continent.

Asia

China is Asia’s leading hemp grower, producing 35-40% of the world’s hemp. Provinces Yunnan and Heilongjiang have defined industrial hemp to have a THC content of no more than 0.3%, and have approved the development of the industrial hemp industry under the guidance of the provincial agricultural science academies. In Yunnan, there is a three-certificate system – the cultivation license, scientific research cultivation license and processing license. The Heilongjiang province mainly produces hemp for the fiber textile industry while the flower and leaf extracts are concentrated in the Yunnan province. Both provinces allow the production of hemp for CBD. However, use of industrial hemp in medicines or foods is not allowed in China. In addition, it is prohibited to use CBD, hemp fruit, hemp seed oil and hemp leaf extract in cosmetics.

Hectares of hemp planted in China surged from 2016 to 2017 by 60% and, with slight fluctuations, continued the upward trend to reach 23,200 hectares in 2021 and 26,500 hectares in 2022, producing 128,000 and 145,000 tons of hemp in 2021 and 2022, respectively. In 2023, hectares of hemp planted rose to nearly 32,000 and then further in 2024 to reach an estimated 38,000.

As of early 2020, there were 158 companies in the Yunnan Province licensed to plant industrial hemp, 101 licensed to process flower and leaf, 14 licensed to extract and process, and 87 companies that have obtained pre-processing approvals. There are around 150 CBD extraction companies in China.

The country exports about 90% of its products to the US, Germany, UK, Netherlands and Japan and has begun growing hemp in three provinces for CBD extraction purposes. Chinese hemp-fiber sales were estimated at $1.2 billion in 2018.

Other countries in Asia – Kazakhstan, Pakistan, India, Thailand, Japan, and South Korea – are actively developing their domestic hemp industries.

In Japan, the primary market for hemp is hemp-derived CBD products which are legal and approved by the health ministry for consumption. However, products can contain no more than 10ppm (0.001%) of THC in oil, 1ppm in edibles, and 0.1ppm in beverages. Though such a low content is difficult to ensure, it is possible and several stores in Japan sell topicals, food, and beverages containing CBD. Euromonitor estimates that Japan’s legal CBD market reached USD$163 million in 2024 with around 530,000 users.

The hemp-derived CBD industry is also big in India where medical hemp products are regulated by the Ministry of AYUSH. Additionally, in November 2021 the Food Safety and Standards Authority of India approved hemp seeds, oil, and flour as food products – significantly simplifying business for companies wishing to produce nutritious products from industrial hemp such as hemp protein powder and cold-pressed hemp seed oil. BOHECO, one of the leading companies in India’s medical and industrial hemp industry, estimates that the general market size for industrial hemp is between $500 million and $750 million annually.

Middle East

In the Middle East, industrial hemp is legal in Israel, Lebanon, and the United Arab Emirates (UAE). Lebanon was the first Arab nation to legalize cannabis for medical and industrial use back in 2020, defining industrial hemp to have no more than 1% THC.

UAE is one of the newest additions to the growing list of countries with legal hemp programs. The UAE Government issued a Federal Decree-Law on December 18, 2025, legalizing industrial and medical uses of industrial hemp and creating a regulatory framework for the industry. THC levels in hemp must not exceed 0.3% and a license is required to cultivate, manufacture, import, or export hemp and hemp products.

Source: hempcbdbusinessplans.com

How Can HempCBDbusinessplans Templates Help Start or Grow Your Hemp CBD Business?

The global regulatory landscape for hemp CBD continues to evolve, creating both opportunities for starting a business or growing an existing one, and complexities in navigating diverse laws and restrictions. Regardless of location, a well-structured business plan remains essential – not only to ensure compliance but also to secure funding and demonstrate a clear path to sustainable growth. It will also help you understand how much money it will take to start a hemp CBD business and how much profit it could make.

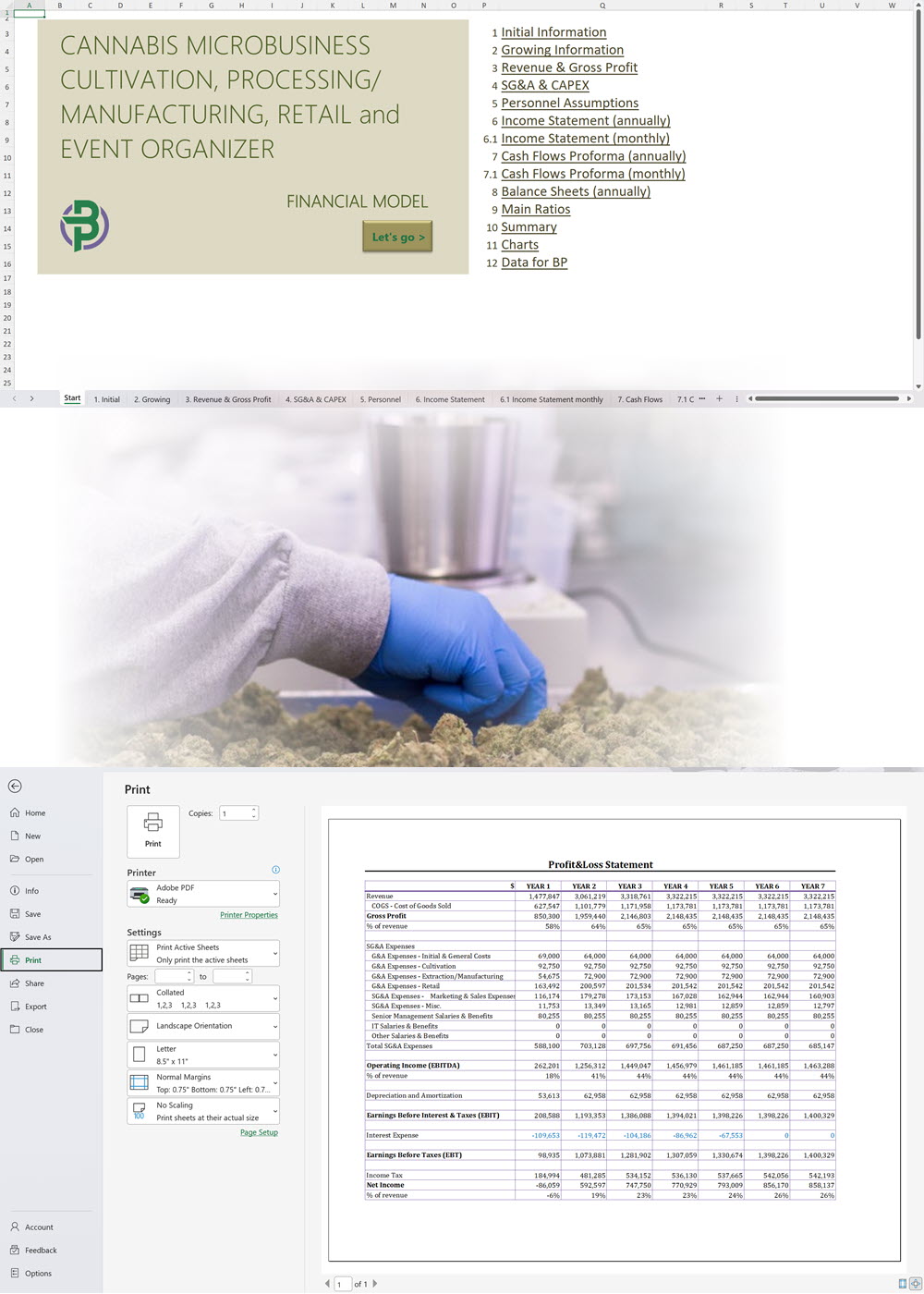

Our complete hemp CBD business plan template package is everything you need to create a professional business plan for a hemp CBD business with expert financials and projections. A complete hemp CBD business plan template package includes:

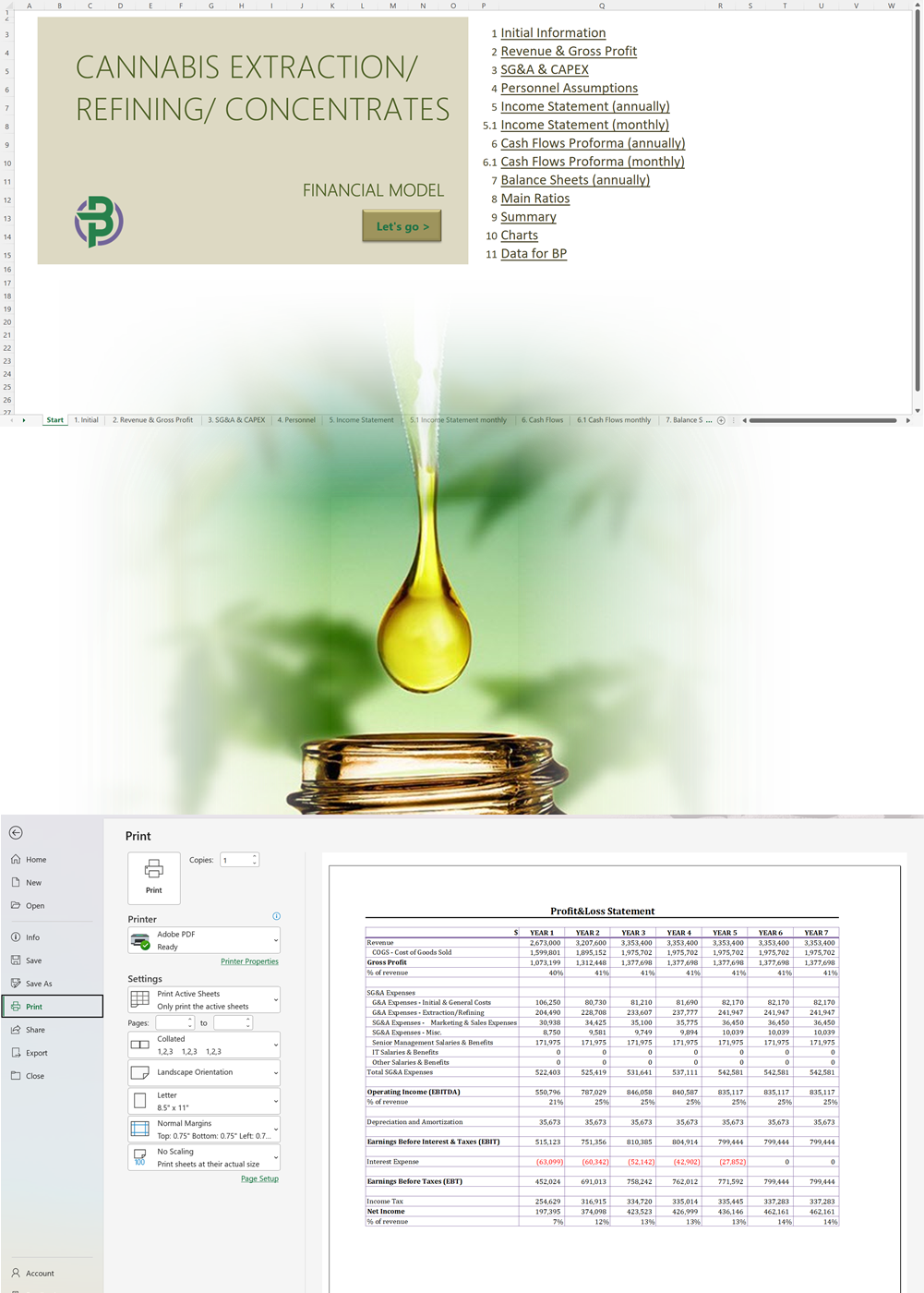

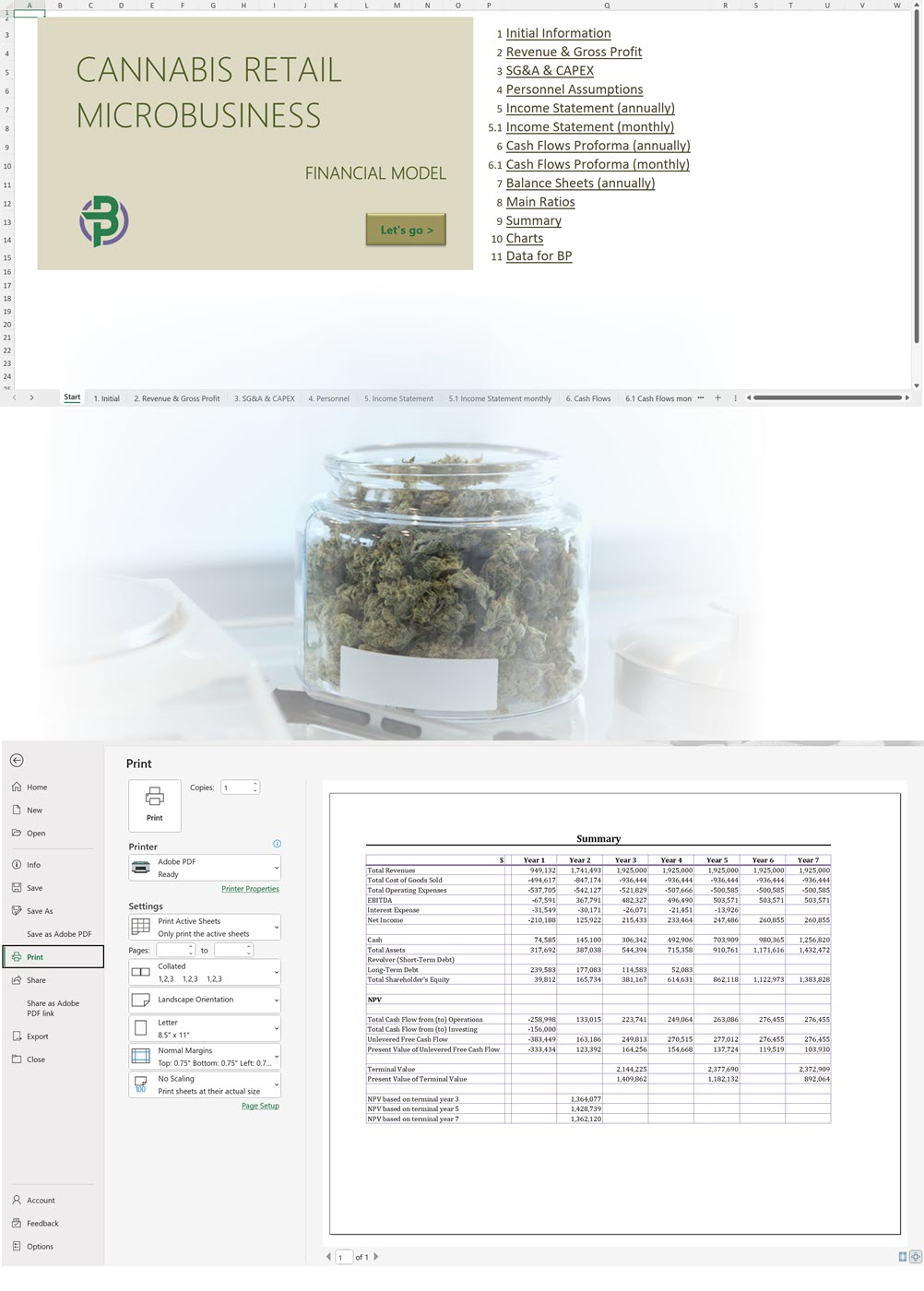

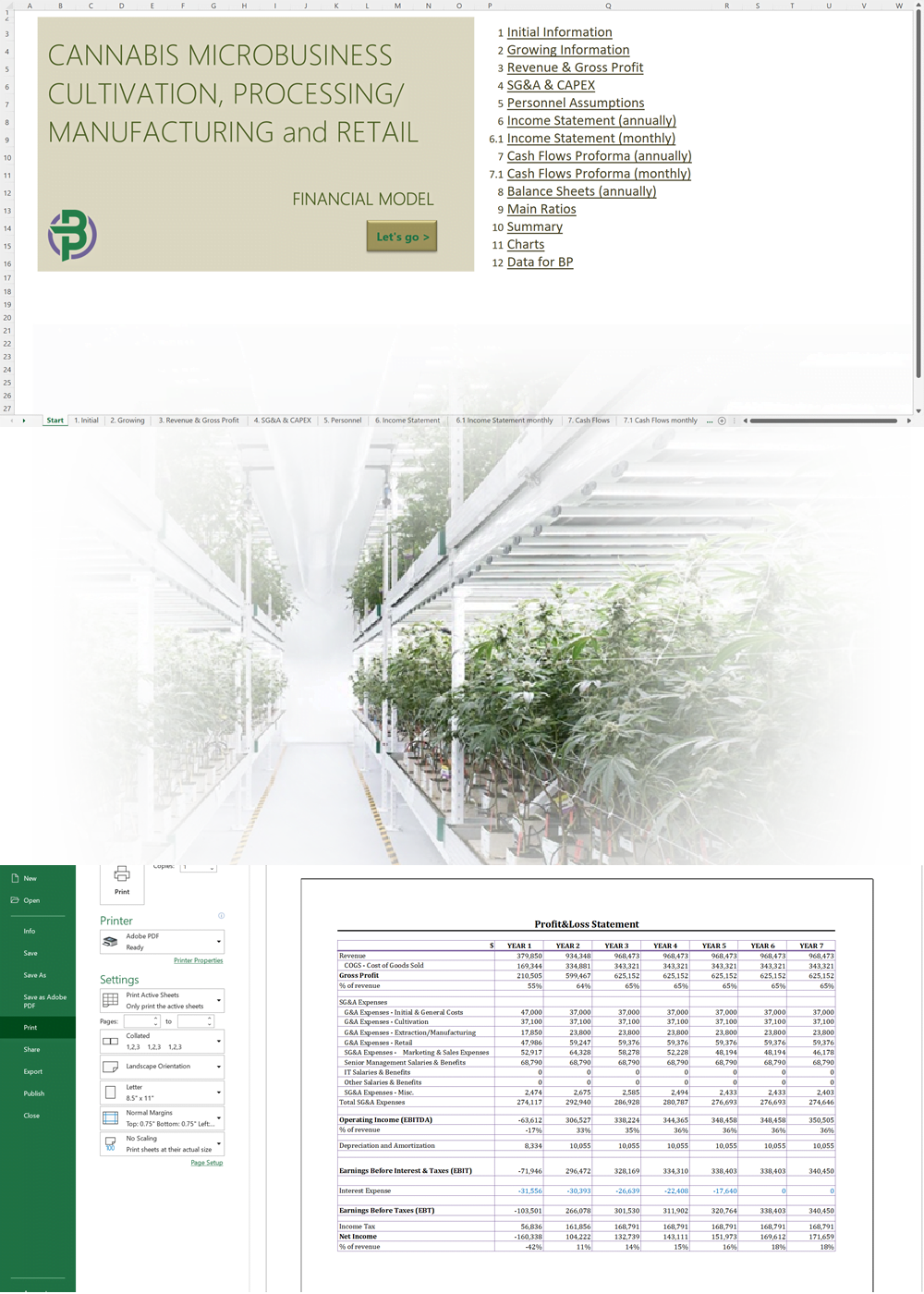

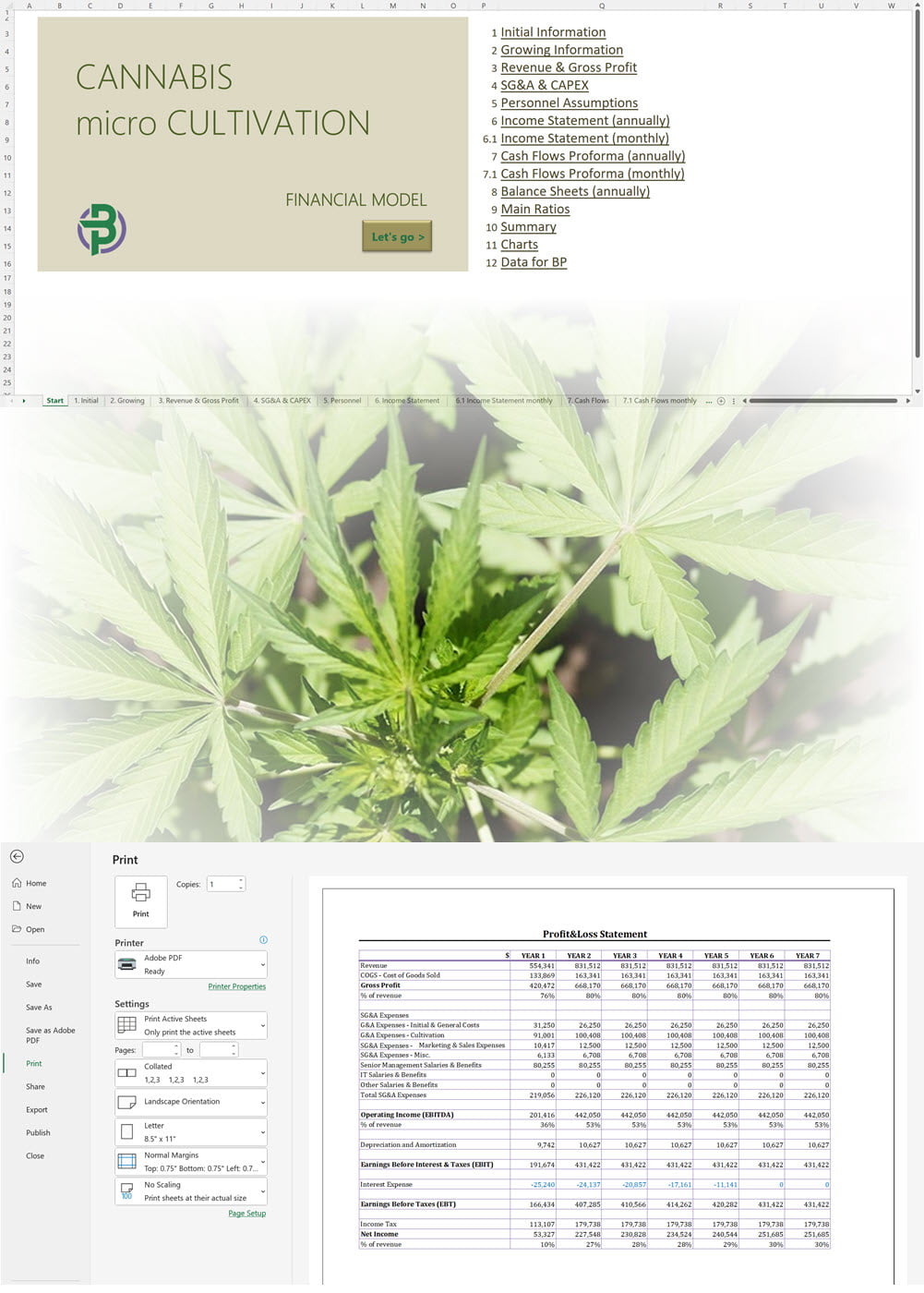

- Excel Financial Model: change variables and immediately see the impact, break down operational and capital costs, know how much it will take to get into the business and the potential profits.

- Word Business Plan: value proposition, market analysis, marketing strategy, operating plan, organizational structure, financial plan and more.

- PowerPoint Pitch Deck: provide a quick overview of your hemp CBD business plan.

Global Hemp Market Infographics

'70% ready to go' business plan templates

Our hemp/CBD financial models and business plan templates will help you estimate how much it costs to start and operate your own hemp/CBD business, to build all revenue and cost line-items monthly over a flexible seven year period, and then summarize the monthly results into quarters and years for an easy view into the various time periods. We also offer investor pitch deck templates.

For more information on the hemp industry, visit hempcbdbusinessplans.com.

Hemp/CBD Business, Legalization and Opportunities in the U.S.

Hemp/CBD Business, Legalization and Opportunities in Canada

Hemp/CBD Business, Legalization and Opportunities in Europe

Hemp/CBD Business, Legalization and Opportunities in Australia

Hemp/CBD Business, Legalization and Opportunities in New Zealand

Hemp/CBD Business, Legalization and Opportunities in Africa

Hemp/CBD Business, Legalization and Opportunities in South America

Our Templates

Cannabis Retail Microbusiness Business Plan Template

Price range: $75.00 through $275.00

Cannabis Cultivation, Extraction, Manufacturing, Distribution, Retail and Microbusiness Business Plan Template

Price range: $75.00 through $500.00

Cannabis Micro Cultivation Business Plan Template

Price range: $75.00 through $300.00

Cannabis Cultivation Business Plan Template

Price range: $75.00 through $350.00

Cannabis Microbusiness Cultivation and Manufacturing Business Plan Template

Price range: $75.00 through $350.00

Vertically Integrated Cannabis Business Plan Template

Price range: $75.00 through $500.00

Cannabis Microbusiness Business Plan Template for Cultivation + Extraction + Manufacturing + Wholesale + Retail + Services

Price range: $75.00 through $500.00

Cannabis Transportation Business Plan Template

Price range: $75.00 through $275.00

Cannabis Cultivation, Extraction and Manufacturing Business Plan Template

Price range: $75.00 through $450.00

Hemp Cultivation and CBD Oil Extraction and/or Fiber Products Business Plan Template

Price range: $75.00 through $350.00