Your Roadmap to Cannabis Business Funding

- Developments and challenges of cannabis business financing.

- Finance from financial institutions.

- Cannabis grants and financial assistance from the government.

- Finance from private lenders.

- Finance from private investors.

- How to secure finance for your cannabis business?

Developments and Challenges of Cannabis Business Financing

One of the major challenges in the cannabis industry both for start-ups and for established businesses is finding financing. The ongoing regulatory and legal complications surrounding the industry – such as the federal prohibition in the US – make financial institutions hesitant to provide funding.

In 2014, the US Treasury Department published guidelines that explained that banks may work with cannabis businesses as long as they verify their state licenses and file Suspicious Activity Reports (SARs) for every transaction they make. These requirements are both expensive and inconvenient to comply with and therefore discouraged financial institutions from dealing with cannabis businesses.

The Safe Banking Act, first introduced in 2013, aims to provide federal protections for banks that offer banking services to cannabis businesses, expanding access to credit. The Safe Banking Act was enhanced to create the SAFER Banking Act (Secure and Fair Enforcement Regulation Banking Act) – in addition to the changes mentioned above, this Act includes greater protection of cannabis-related account holders and depositors, prohibits federal regulators from terminating or limiting deposit insurance because a financial institution has cannabis-related clients, and has more clarity regarding lending. The SAFER Banking Act passed the Senate Banking Committee in September 2023 and is still waiting for a Senate floor vote. If this Act does pass this time and is signed into law, this will significantly improve cannabis businesses’ access to full-service banking and capital.

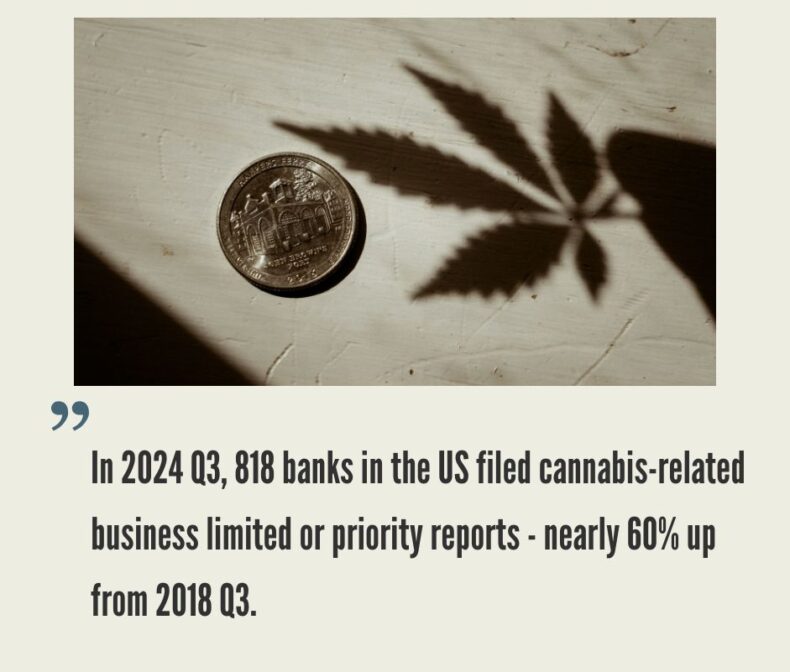

Despite these challenges, as the global acceptance of cannabis increases, access to financing for cannabis businesses is improving as well. There are now financial institutions who are willing to provide finance to cannabis businesses as well as grants and loans offered in some countries and US states intended to boost the cannabis industry. In recent years, more and more smaller banks have become willing to serve the cannabis industry with the platform FlowHub listing several examples. According to quarterly data from the US Department of the Treasury, in 2024 Q3, 818 banks filed cannabis-related business limited or priority SARs – nearly 60% up from 2018 Q3 and more than 5 times the number of SARs that were filed in 2014 Q3.

Cannabis businesses need financing for a number of reasons:

- Cannabis equipment financing.

- Cannabis real estate financing.

- Cannabis inventory financing.

In this article, we outline the different sources of finance available for your cannabis business.

Financial Institutions

Lines of Credit

You make an agreement with a financial institution to borrow up to a certain limit. It comes with an annual percentage rate which is the rate at which you will have to pay interest on the amount you borrow. This funding option offers flexibility as you can decide how much you need to borrow at any time as long as you do not exceed the maximum limit established in the agreement.

Term Loans

Fixed-payment loans with fixed rates which provide an injection of a lump sum of capital into your business. This amount must be repaid in regular installments, as outlined in the contract. These loans are most appropriate when you are just starting up your business or for investments such as equipment upgrades or renovations.

Commercial Real Estate Loans

Every cannabis business must acquire property, whether it is a retail store for a dispensary or a growing facility for cultivation. In some US states, an applicant for a cannabis license is required to secure a location prior to their license being approved. This raises the need to seek finance to purchase property and commercial real estate loans are meant for exactly this. Similar to a residential mortgage, the property purchased is a collateral for the loan.

Cannabis Grants and Financial Assistance from the Government

Some US state programs for cannabis licensing and regulation offer grants to certain categories of cannabis businesses. Canada also provides grants and contributions to its cannabis businesses through various programs including: the Sustainable Canadian Agricultural Partnership program, the Industrial Research Assistance Program, the National Research Council Canada, and the Scientific Research and Experimental Development tax incentives. Canada is actively providing assistance to its cannabis businesses through these programs as a search of its Grant and Contributions data by the keyword “cannabis” reveals that since 2018, more than CA$170 million worth of funding has been provided to cannabis businesses.

The infogram below shows the US states that currently offer financial assistance or grant programs:

Private Lenders

Private lenders are individuals or entities that provide loans to businesses in exchange for repayment with interest. Since the beginning of the legalization of cannabis, many startups relied on financing from private money lenders. The increase in the number of private lenders in recent years has resulted in greater competition between lenders and more favorable loan terms for cannabis businesses. According to Bloomberg Law, borrowers can now secure interest rates from 8% to 18% compared to the previous higher rates of 25% and more. For equipment-based loans, interest rates can even be 3.5%.

Loans will usually require security interests – assets that the lender will gain possession of in the event that the borrower cannot continue making repayments. You must be prepared to offer as security interests your real estate, physical assets or other assets that can be pledged legally. Another possible requirement may be a corporate or personal guarantee – an agreement by someone other than the borrower of the borrower’s obligations. If the borrower cannot make a repayment, the guarantor will have the obligation to make the repayment in place of the borrower.

Hard Money Lenders

Typically private individuals or small companies that lend money based on the value of collateral, such as real estate. They usually look for high-value collateral such as property or equipment, and grant loans for short periods of time – 6 months to 3 years.

Peer-to-Peer Lenders

Platforms that connect individual investors with borrowers, bypassing traditional financial institutions. They look for a good credit score and a solid business plan.

Family Offices or High-Net-Worth Individuals

This type of private lenders provide loans to businesses they believe in. It is important to gain their attention by having a good idea communicated through a well-structured and clear business plan.

Private Investors

Private investors make an investment in a business, often in the form of equity, and seek to make a return on their investment. Investors typically look at management skills, a clear business plan outlining the business proposal, high-quality financial forecasts, and a plan for sustainable, strategic growth.

Angel Investors

These are wealthy individuals who invest using their own capital, usually at early stages of a startup. They may also provide mentorship and strategic guidance alongside capital. Angel investors typically look for high growth potential, a passionate management team with a clear vision, and are willing to take on more risk in exchange for higher returns.

Venture Capital Firms

A venture capital firm pools money from multiple investors to fund high-growth startups. They look for disruptive ideas with market potential that lead to scalability and profitability.

Private Equity Firms

They usually invest in more mature companies by acquiring controlling stakes. They may also provide growth capital for the purpose of expanding operations. Private Equity firms usually look for an established track record (proven profitability and operational stability) and alignment with the firm’s portfolio or investment thesis.

How to Secure Finance for Your Business?

A business plan is a non-negotiable for securing funding from a financial institution, investor or a governmental organization. A business plan offers insight into funding utilization which will help to convince the finance provider that you will be able to repay the loan or provide them with an attractive return.

Our complete cannabis business plan template package is everything you need to create a professional business plan for a cannabis business with expert financials and projections. A complete cannabis business plan template package includes:

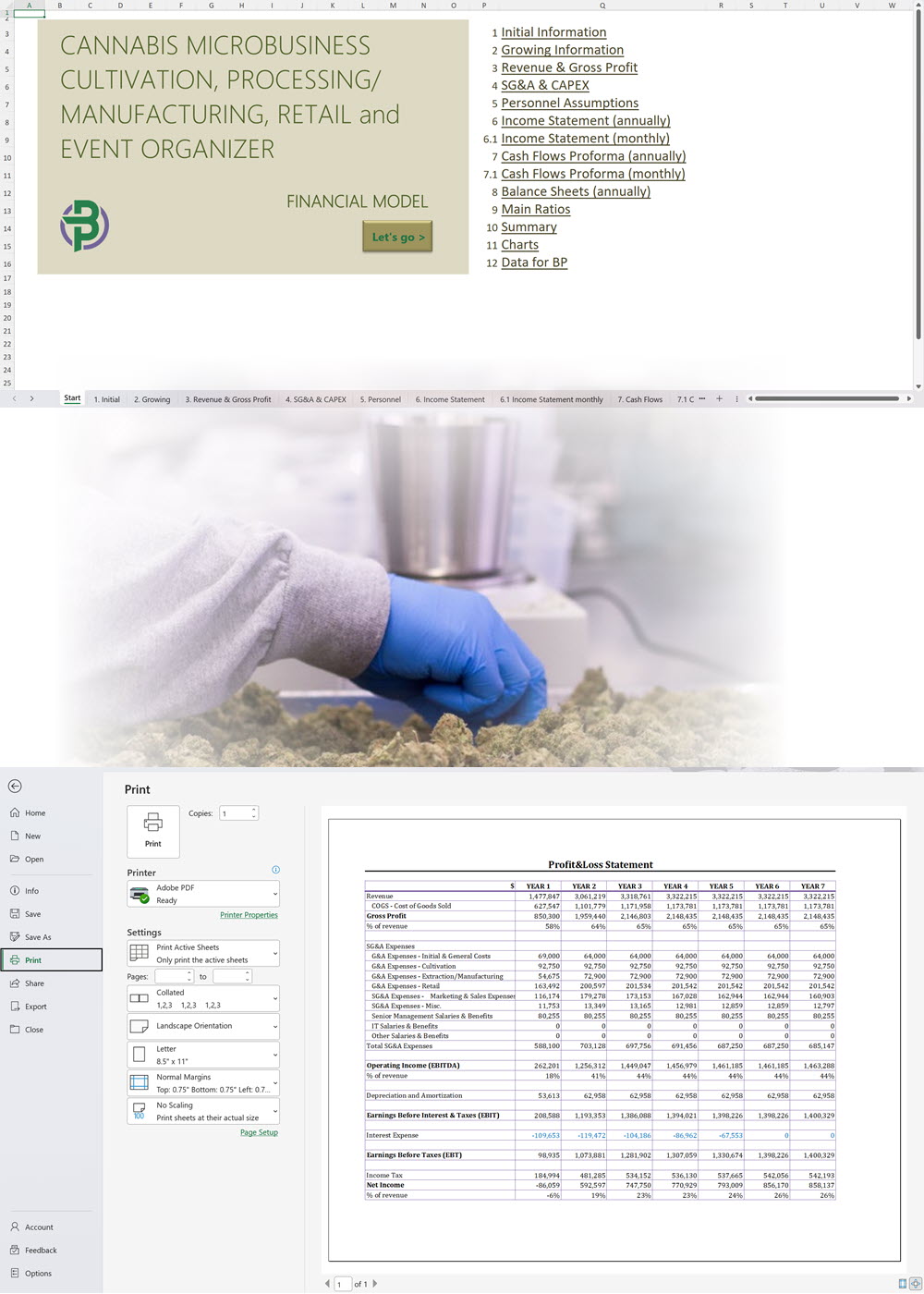

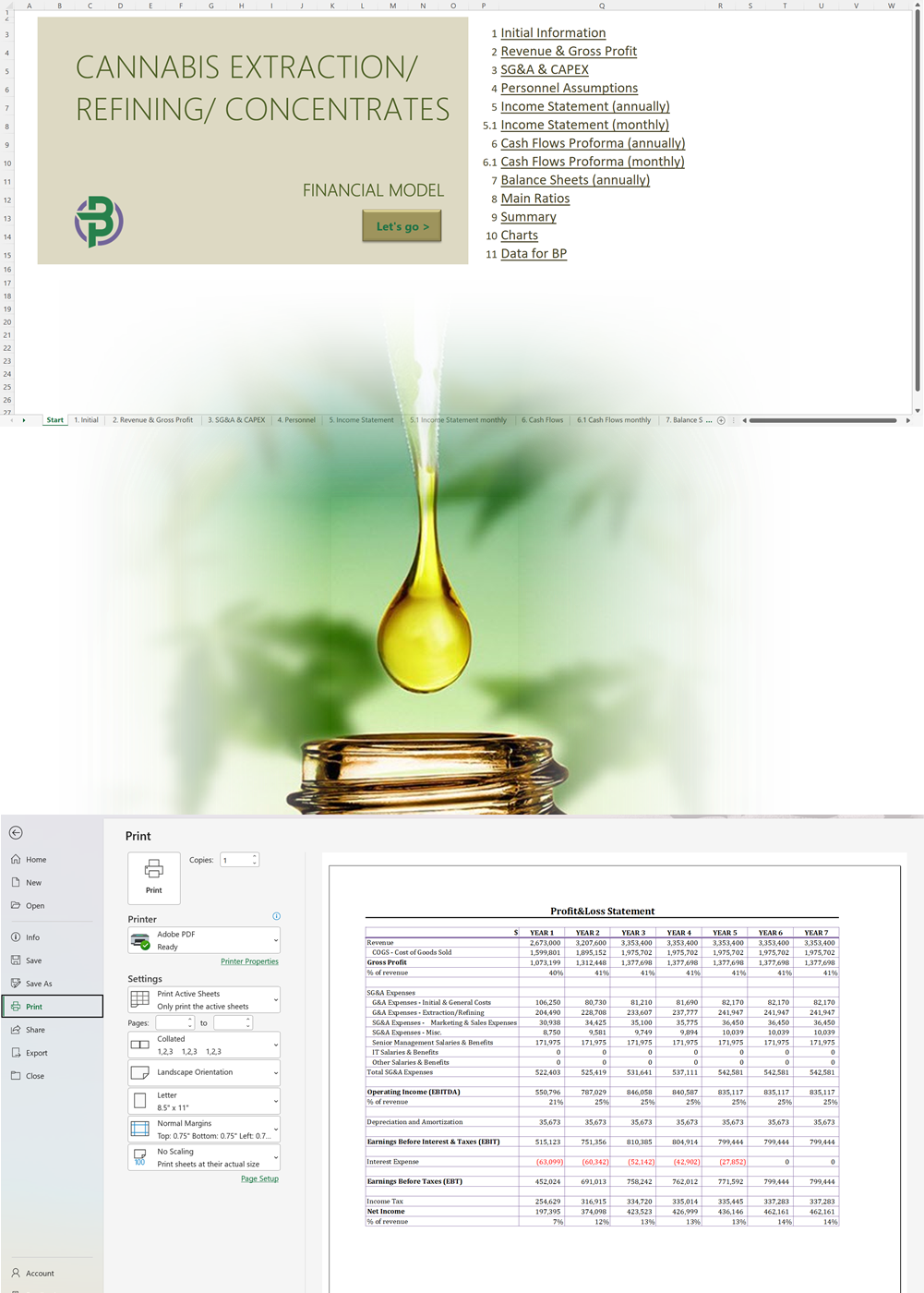

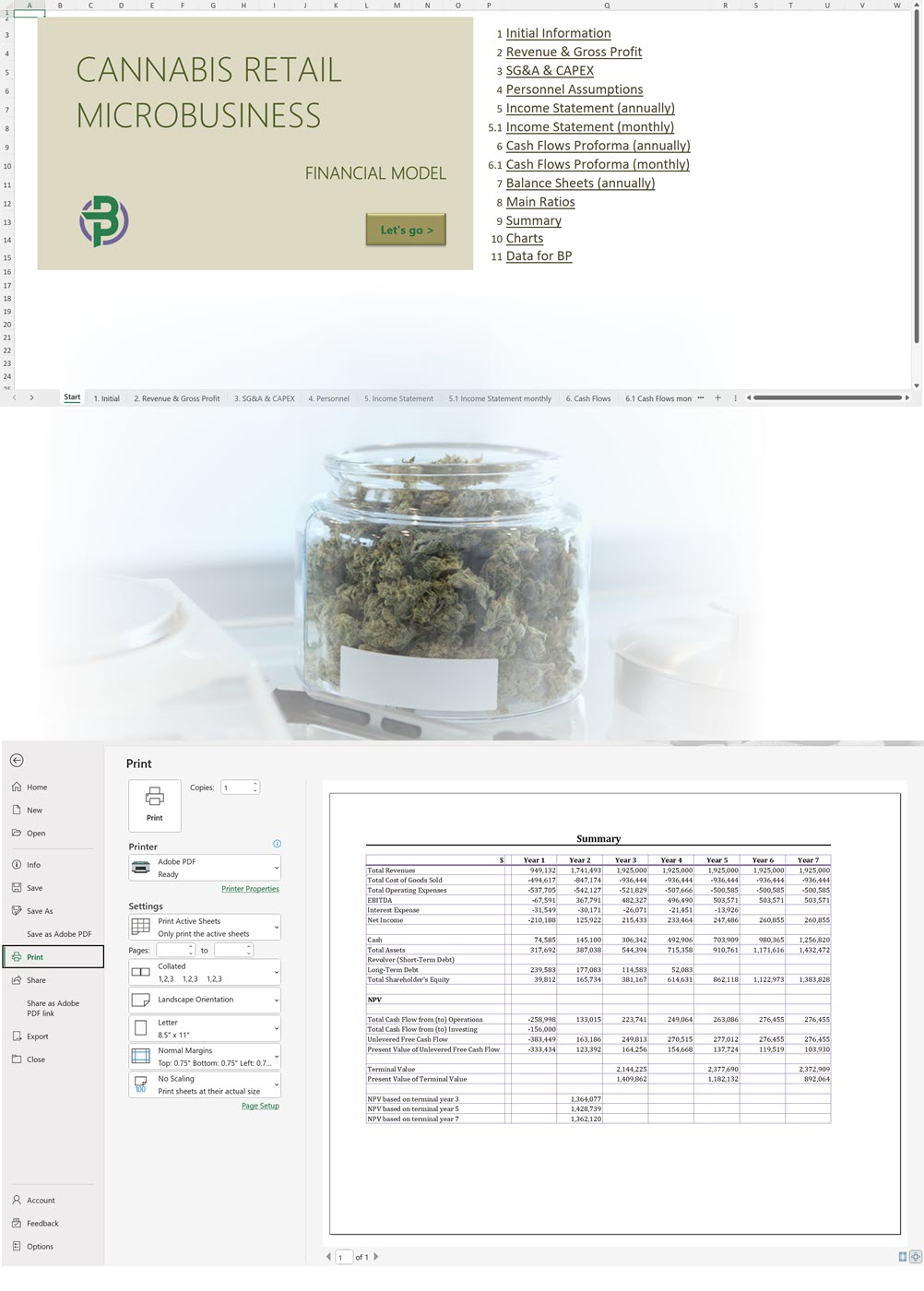

- Excel Financial Model: change variables and immediately see the impact, break down operational and capital costs, know how much it will take to get into the business and the potential profits.

- Word Business Plan: value proposition, market analysis, marketing strategy, operating plan, organizational structure, financial plan and more.

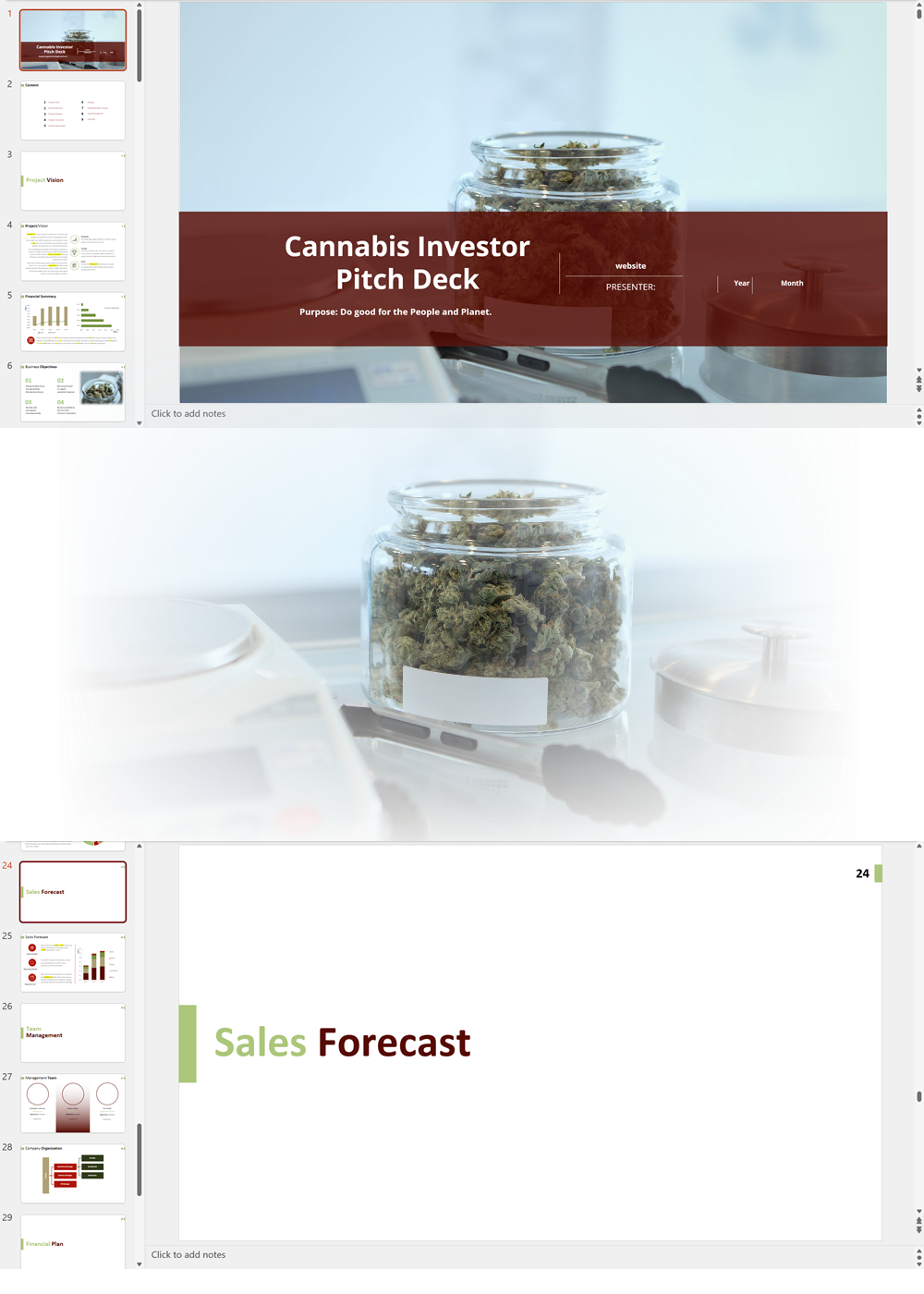

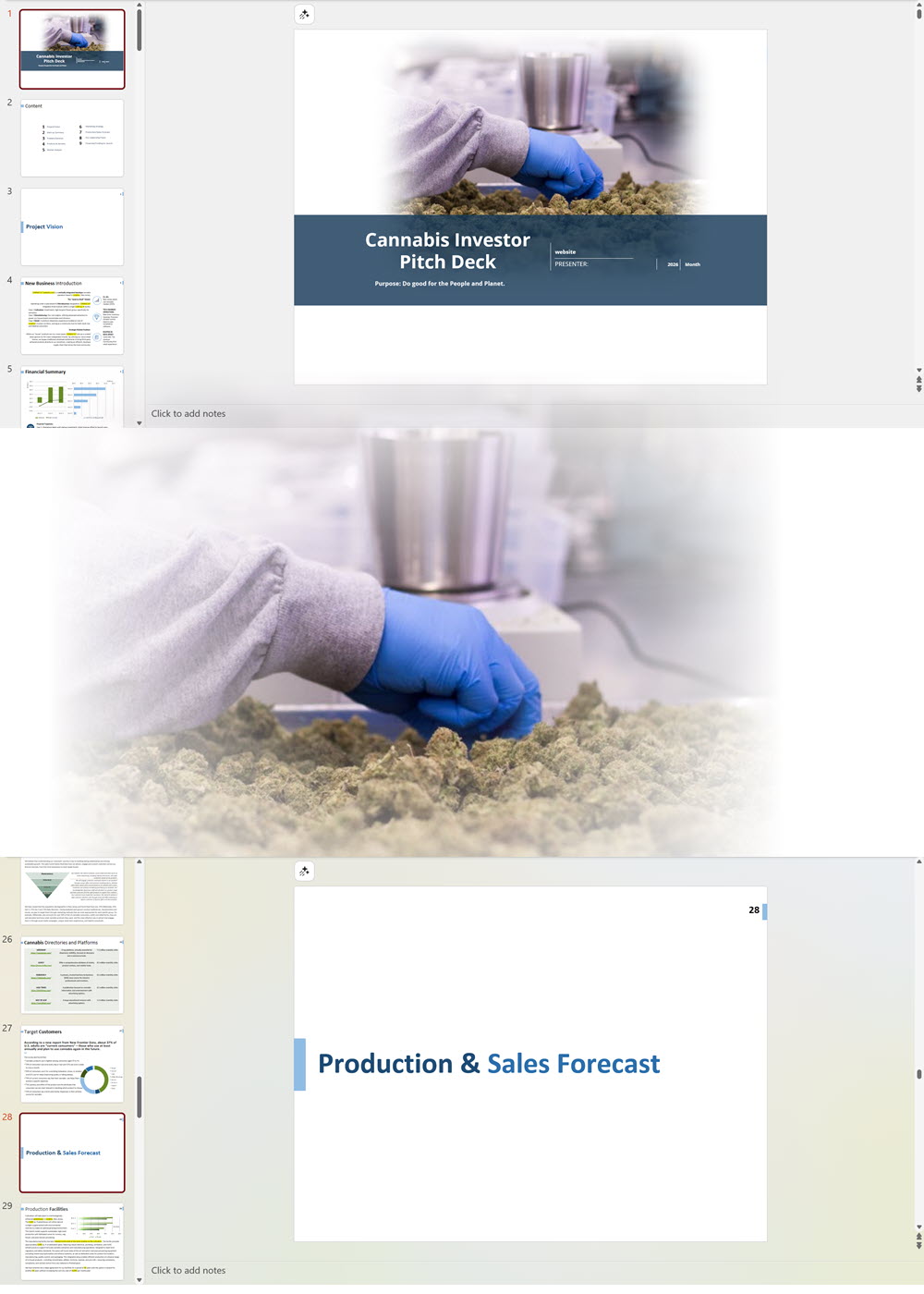

- PowerPoint Pitch Deck: provide a quick overview of your cannabis business plan.

Our cannabis financial models and cannabis business plan templates will help you estimate how much it costs to start and operate your own cannabis business, to build all revenue and cost line-items monthly over a flexible seven year period, and then summarize the monthly results into quarters and years for an easy view into the various time periods. We also offer investor pitch deck templates.'70% ready to go' business plan templates

In addition to the business plan, when applying for a loan or a grant, the following documents will likely have to be provided:

- Capitalization table: a list of your company’s owners and their percentage of ownership.

- Certification of EIN/TIN or tax return.

- Cannabis license.

- Operating agreement or company bylaws.

- Property title or lease.

- Secretary of State filing or Certificate of Good Standing.

- Certificate of Insurance.

According to the law firm Harris Sliwoski, private investors in particular will likely ask for additional documents from categories which include:

- Corporate Records

- Securities Issuances

- Financing Documents

- Material Contracts

- Management and Employees

- Financial Information

- Sales and Marketing

- Real Property

- Intellectual Property

- Government Regulations and Compliance

- Insurance

- Taxes

Best Selling Templates

Cannabis Cultivation Business Plan Template

Price range: $75.00 through $350.00

Select options

This product has multiple variants. The options may be chosen on the product page

Cannabis Dispensary Investor Pitch Deck Template

$75.00

Select options

This product has multiple variants. The options may be chosen on the product page

Cannabis Financial Model All in One

$250.00

Select options

This product has multiple variants. The options may be chosen on the product page

Hemp/CBD business plan templates are available at hempcbdbusinessplans.com.

Our Templates

CBD Store and/or Cafe Lounge Business Plan Template

Price range: $75.00 through $275.00

Cannabis Extraction / Concentrates Business Plan Template

Price range: $75.00 through $350.00

Cannabis Processing/ Flowers/ Pre-rolls/ Extraction/ Manufacturing Business Plan Template

Price range: $75.00 through $350.00

Cannabis Transportation Business Plan Template

Price range: $75.00 through $275.00

CBD Products Retail/Online Store Business Plan Template

Price range: $75.00 through $275.00

Cannabis Edibles Financial Model

$150.00

Cannabis Lounge + Retail Business Plan Template

Price range: $75.00 through $350.00

Cannabis Retail Business Plan Template (with or without Delivery)

Price range: $75.00 through $350.00

Cannabis Edibles Business Plan Template

Price range: $75.00 through $350.00

Cannabis Retail Microbusiness Business Plan Template

Price range: $75.00 through $275.00

Cannabis Cultivation, Extraction, Manufacturing, Distribution, Retail and Microbusiness Business Plan Template

Price range: $75.00 through $500.00

Cannabis Micro Cultivation Business Plan Template

Price range: $75.00 through $300.00