Key Takeaways

- Cannabis law and regulations:

- The Marijuana Enforcement Division (MED, part of the Colorado Department of Revenue) is responsible for licensing and regulating the Medical and Retail Marijuana industries in Colorado.

- Licenses available:

- There are eight types of cannabis licenses in Colorado: cultivator, manufacturer, retailer, hospitality business, hospitality and sales business, business operator, testing facility, and transporter. The state allows vertical integration but does not mandate it.

- Products legal:

- A wide range of cannabis products are available, including dried flower, concentrates, edibles, and more. Adults over the age of 21 can buy and possess up to 1 ounce of cannabis at a time.

- Taxes:

- Retail marijuana is subject to a 15% retail marijuana excise tax, applied to the first sale or transfer from the cultivation facility, as well as a 15% retail marijuana sales tax, which applies to the final sale to the consumer. In contrast, medical marijuana is exempt from the excise tax.

- Market:

- Cannabis consumers spent $1,315 million in 2025, including $1,182 million recreational cannabis sales, according to data from the Department of Revenue’s Marijuana Enforcement Division.

Cannabis Laws in Colorado

Colorado cannabis market has been legal for medical use since 2000 and for recreational use since late 2012. Colorado became the first state to approve 280E deductions in 2014, that allows cannabis companies to deduct business expenses from their state income taxes.

Two new bills, House Bill 1230 and House Bill 1234 created two new business licenses for cannabis tasting rooms and cannabis deliveries starting with medical products in 2020 and recreational to follow in 2021.

On March 30, 2026, SB26-007 – ‘Medical Marijuana Use in Health Facilities’ was signed into law. The bill authorizes (but does not mandate) health facilities such as hospitals to allow patients who are terminally ill and registered in the state’s medical cannabis program to use medical cannabis within the health facility.

Colorado Cannabis Market: Stats and Projections

Colorado’s retail sales in adult-use and medical dispensaries combined grew from $675 million in 2014, to about $2.19 billion in 2020 and $2,229 million in 2021 before declining to $1,769 million in 2022, including $231 million medical and $1,538 million recreational cannabis sales. Cannabis consumers spent $1,529 million in 2023, including $185 million medical and $1,344 million recreational cannabis sales, according to data from the Department of Revenue’s Marijuana Enforcement Division. 2024 brought in around $1,397 million in total sales, including $1,234 million recreational cannabis sales.

In 2025, medical cannabis sales totaled approximately $133 million, while recreational cannabis sales amounted to $1,182 million – representing nearly 90% of total cannabis sales. Cannabis sales averaged $1.72 million per retail location in Colorado’s adult-use market and $0.47 million per location in the medical channel.

Colorado cannabis prices have steadily declined since 2021, hitting historic lows in 2025, which is the primary driver behind the overall drop in sales revenue. Despite the overall sales decline, the market is showing signs of stabilization, with product innovation driving growth in categories like pre-rolls and cannabis beverages, and newly legalized cities such as Colorado Springs contributing to localized sales increases and higher dispensary foot traffic.

Medical:

- Dispensaries – 284 (306)

- Cultivators – 218 (259)

- Manufacturers – 142 (170)

- Testing – 7 (7)

- Transporters – 4 (8)

- Delivery – 4 (6)

- Retail Stores – 688 (659)

- Cultivators – 487 (535)

- Manufacturers – 215 (242)

- Testing – 7 (7)

- Transporters – 10 (18)

- Delivery – 14 (25)

- Hospitality – 13 (16)

Recreational: 550,000 – 650,000

Recreational: $1,182 million (versus $1,234M in 2024 and $1,344M in 2023)

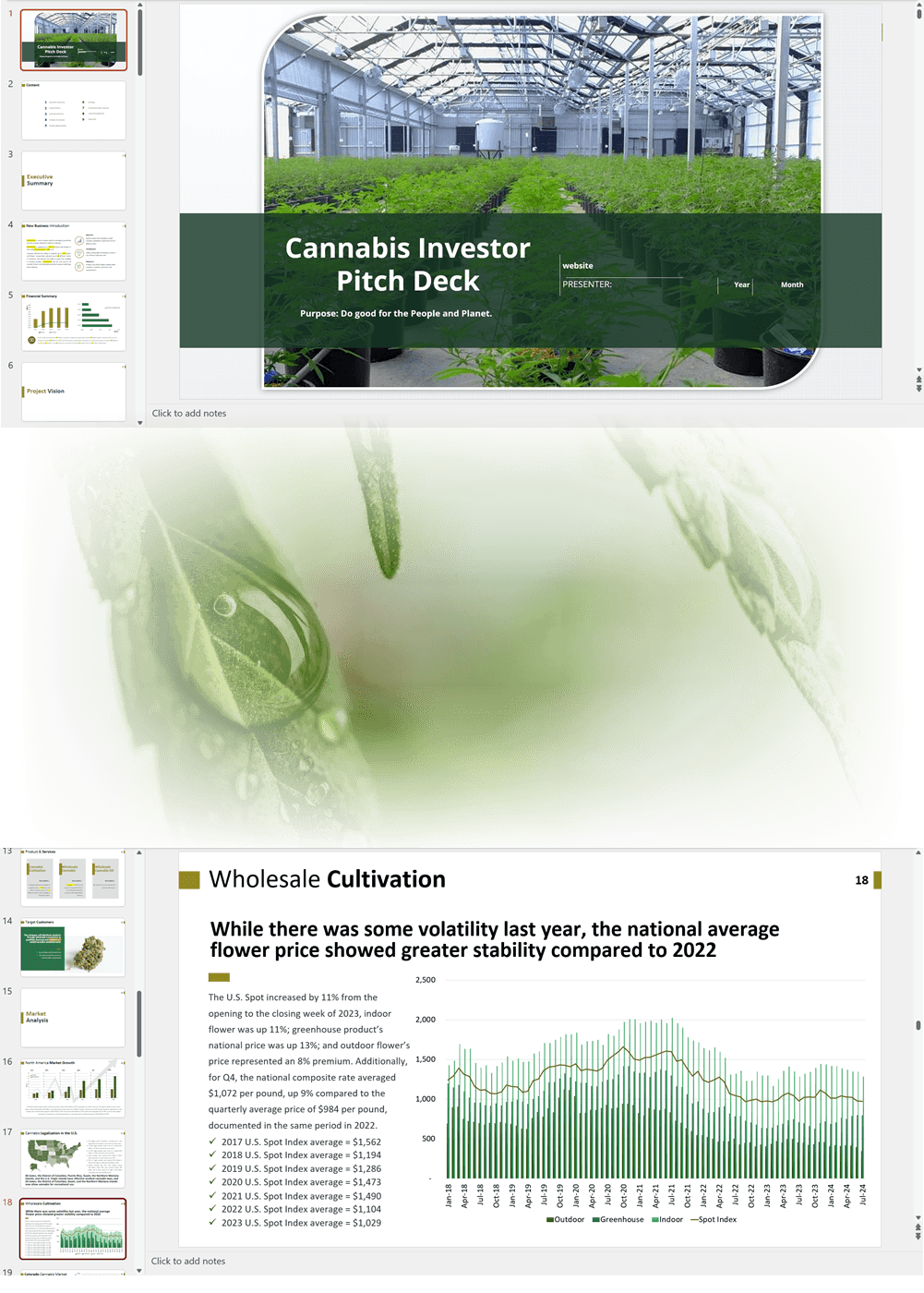

Demand for Cannabis Concentrates in Colorado

In 2014 when adult-use just launched in Colorado, over 70% of sales came from dried flower; in 2016, that was down to 55%. In contrast, concentrate sales were $20 million in 2014, or 13% of sales. By the end of 2016 they had jumped to $85 million and 24% of sales. Edibles (including candy, beverages, tinctures, and all food) more than tripled during the same period, from $17 million to $53 million, moving from 11% to 13% of sales. Vape pens and vape products, candy, and other portable and convenient methods of consumption are especially popular with Colorado consumers.

The contribution of sales from flower dropped to less than 50% in 2018 and to 40% in 2024 and increased from concentrates to 32% and 39% correspondingly in Colorado’s cannabis industry.

Colorado Cannabis Market Infographics

'70% ready to go' business plan templates

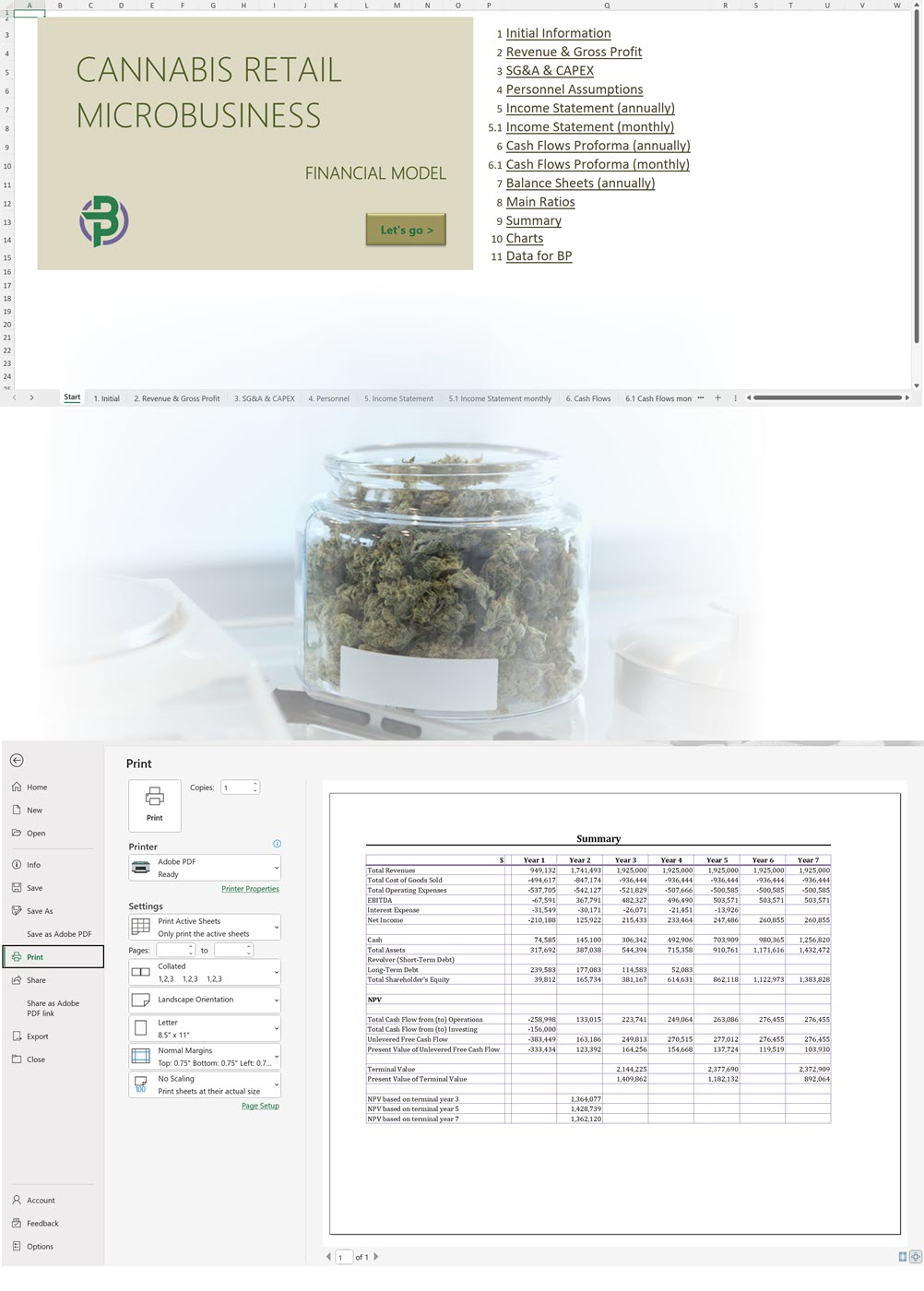

Our cannabis financial models and cannabis business plan templates will help you estimate how much it costs to start and operate your own cannabis business, to build all revenue and cost line-items monthly over a flexible seven year period, and then summarize the monthly results into quarters and years for an easy view into the various time periods. We also offer investor pitch deck templates.

Best Selling Templates

-

Cannabis Cultivation Business Plan Template

Price range: $75.00 through $350.00 Select options This product has multiple variants. The options may be chosen on the product page -

Cannabis Dispensary Investor Pitch Deck Template

$75.00 Select options This product has multiple variants. The options may be chosen on the product page -

Cannabis Financial Model All in One

$250.00 Select options This product has multiple variants. The options may be chosen on the product page

Hemp/CBD business plan templates are available at hempcbdbusinessplans.com.

Our Templates

CBD Store and/or Cafe Lounge Business Plan Template

Price range: $75.00 through $275.00

Cannabis Extraction / Concentrates Business Plan Template

Price range: $75.00 through $350.00

Cannabis Processing/ Flowers/ Pre-rolls/ Extraction/ Manufacturing Business Plan Template

Price range: $75.00 through $350.00

Cannabis Transportation Business Plan Template

Price range: $75.00 through $275.00

CBD Products Retail/Online Store Business Plan Template

Price range: $75.00 through $275.00

Cannabis Edibles Financial Model

$150.00

Cannabis Lounge + Retail Business Plan Template

Price range: $75.00 through $350.00

Cannabis Retail Business Plan Template (with or without Delivery)

Price range: $75.00 through $350.00

Cannabis Edibles Business Plan Template

Price range: $75.00 through $350.00

Cannabis Retail Microbusiness Business Plan Template

Price range: $75.00 through $275.00

Cannabis Cultivation, Extraction, Manufacturing, Distribution, Retail and Microbusiness Business Plan Template

Price range: $75.00 through $500.00

Cannabis Micro Cultivation Business Plan Template

Price range: $75.00 through $300.00

Cannabis Cultivation Business Plan Template

Price range: $75.00 through $350.00